Water Damage Series – Part 11: Finances

The way of the world is: money is the grease that makes things happen. A cynic would say this is because people are greedy. I am not a cynic. Even though water disaster mitigation companies deal with water damage and some devastating circumstances, your best mitigation companies are not cynical either.

Because we’ve seen what it takes to recover from a water disaster, we know that recovery is very realistic. We’ve seen what a disaster looks like, we’ve done the cleanup and restoration. We know what it takes to restore a property and therefore know the reason for optimism.

Money pays for the replacement materials and pays for labor. Everything costs money. That’s why having the right amount of money and having it worked out as early as possible is best. It will make your recovery from water damage happen more smoothly.

The Recovery Team

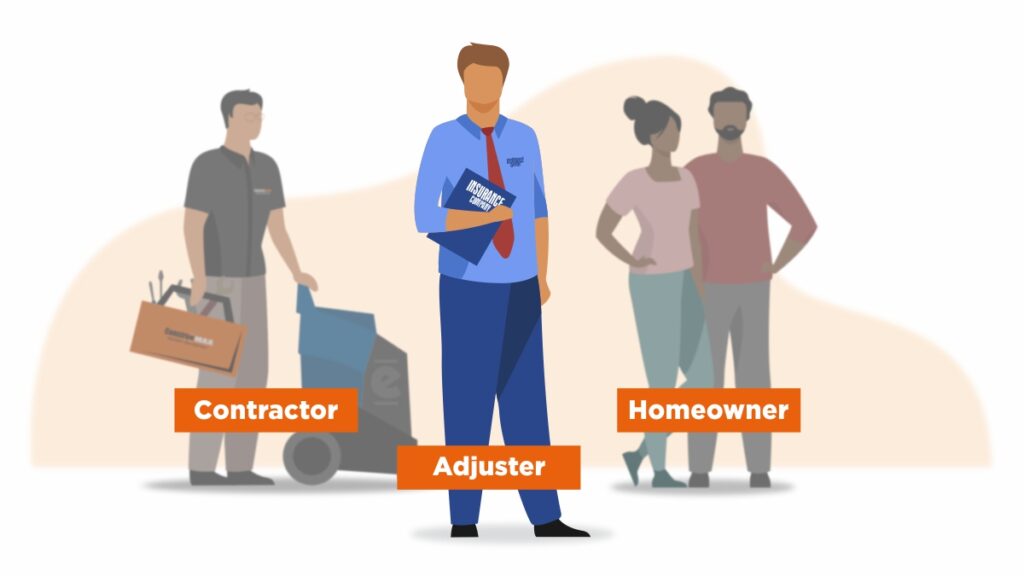

As a reminder from the last post, when it comes to recovery there are three primary players in the process. They are:

1. The injured party (in our context the property owner)

2. The financially responsible party

3. The people performing the labor to restore the property

This time we’ll focus on the financially responsible party. We’ll focus on the insurance company because if you don’t have insurance it’s pretty straight forward, you make all financial decisions.

The Financially Responsible Party

In most cases the financially responsible party is either you, the property owner, or an insurance company. This team member makes recovery possible.

If you do not have property insurance, then any work that needs to be done to restore your property is your responsibility. If it cost $3,500 to clean up the water and damaged materials and another $3,500 to replace it, then that cost is borne by you. That can be hard to swallow for most people, and most can’t just write a check for it. That is why mortgage companies require insurance.

The benefit of being personally responsible is that you don’t have to get anyone else involved to just solve the problem. You hire someone to do the cleanup and restoration the way you want it done, and you move on.

When you have insurance, you’re asking someone else to pay. They are going to investigate before they pull out their checkbook.

Insurance

If the disaster warrants filing a claim an adjuster will be assigned to investigate. Their responsibility is to determine what is covered and provide you with the financial resources to restore your property. This is the settlement they offer you to resolve the claim.

Quick Aside

The adjuster will strictly execute the policy according to the terms that both you and the insurance company agreed to. They will give you no less money than you are entitled but will not provide any more money than you are entitled either.

Having said that, everyone involved is human, and humans are prone to bias, even when making every effort to be fair. The adjuster works for the insurance company. They represent them in the negotiation of the settlement.

They are also obligated to follow the law and the terms of the policy. That means that even if the insurance company doesn’t want to pay, the adjuster will hold them to their obligation. But if a policy doesn’t cover a particular loss (or part of a loss) then the obligation is to ensure the insurance company isn’t held financially responsible for something not previously agreed (i.e. via the policy).

This relationship between the insurance company and the property owner may seem to be at cross purposes, but in reality, everyone just wants to have a fair outcome. If there is disagreement between you and your insurance company, there are options for hiring someone to represent you in this negotiation. It can be a licensed attorney or a public adjuster. Your mitigation and construction companies cannot do that. They can talk with your adjuster, provide information, but they cannot represent you or speak on your behalf.

Insurance Companies Paying for Restoration

When there is a legitimate insurance claim the insurance adjuster that is assigned to the job will investigate the claim. In doing so they will seek to determine:

- The cause of the water damage

- The extent of the damage (what was damaged and how badly)

- If the water damage is covered in the terms of the policy and if so, how much

- The limits stipulated in the policy

- If all of the applicable conditions of the policyholder have been met

- What it will cost to return the property to pre-loss condition

With this information, they can determine what the next actions are. Insurance companies have to follow strict laws about responding to claims and paying for the claims. There are penalties for not paying a claim in a timely manner, so they try to move fast to not run afoul of those legal requirements.

It is very common for insurance companies to write checks for damage only to find, during the repair process, that the extent of the damage is greater than what could have been seen during an inspection. They are accustomed to working with supplements to initial claims.

Insurance companies want you to be a happy customer who only speaks highly of their help during this hard time. So they listen to you and try to be fair. Work with them as best you can to get a good outcome.

Mitigation Is About Preventing Further Damage

Remember the insurance policy condition mentioned in the last post about preventing further damage? There is a really good reason for that. Early mitigation can prevent greater damage and greater expense.

Here is a hypothetical example with round numbers to give you an idea. For the sake of simplicity, we will ignore all deductibles. We’ll come back to that in the end.

Suppose you have a water pipe burst that causes damage to your home. You take care of it immediately and the cost of mitigation is $1200. That’s a chunk of change that can put a dent in your wallet. For simplicity sake, suppose the cost to replace the carpet and carpet pad after it was destroyed is another $1200. That’s $2400 to restore your home back to pre-loss condition.

But What if You Wait?

Now suppose that you didn’t do anything about the burst pipe right away, or you decided to mop up the water yourself and use box fans to try to dry it out. As a result, the carpet didn’t dry very well at all. Mold started to grow, not only in the carpet, but because of all the moisture, it grew on walls and behind the baseboards as well. You realized this became a bigger issue and filed a claim.

Your insurance company recommended a mitigation company to address the damage. They have to not only remove the carpet and place drying equipment, but because of the mold, they have to remove the baseboards and cut off the bottom two feet of drywall around the affected area. It takes longer to dry because the wood has absorbed more of the water, so the equipment is there for a longer amount of time.

The cost of the mitigation has clearly gone up, higher than the original $1200, and the repairs are no longer just replacing carpet and carpet pad. You also have to patch the drywall and replace the baseboards. Of course, you won’t be satisfied with the drywall not matching the rest of the room. To match, the whole room will need to be painted, even if the drywall patch is only 9 square feet because fresh paint will never match the existing paint.

So, what is the new cost of the repairs? Double, triple, even more? Well, it has the potential to be much, much more.

Consequences

The consequence of NOT doing mitigation right away could be extremely expensive, and if you’re expecting the insurance company to pay for it, they expect you to do what you can to prevent further damage.

If you do not do your part to act quickly to mitigate water damage (or any covered damage) they may determine that you didn’t fulfill your obligation to take reasonable measures to prevent further damage. If they make that determination, they could deny a portion of the claim or even deny the claim completely. Now the whole cost is yours to pay, or you take them to court and prove that you did fulfill your obligation in hopes that a court will order them to pay.

For this reason, the insurance companies want you to hire a mitigation company, and they will pay these costs, to prevent further damage.

Tied to this policy condition that requires you to prevent further damage is the condition to maintain good records and receipts. Even if your mitigation company communicates directly with the insurance company for billing, you still need to make sure you have records of everything that happens.

Of course, as always, verify all coverage with your policy as written and seek clarification from an attorney or your insurance agent, because just as every loss is different, every policy can have its own unique differences.

The Right Order of Things

To make sure you get the most of your insurance policy (you are paying premiums after all) is to:

- Arrest the water damage as soon as it is discovered. You do this by calling in a water damage expert like Construemax

- Contact your insurance company about the water loss

- Hire a contractor to repair the damage and build back any part of the property that had to be removed because of damage.

You can hire whomever you want for the mitigation and repairs. If you call your insurance company first, they might be able to help you find a mitigation company. However you do it, don’t wait to do either of these first two things. The earlier you mitigate the lower the final cost for you or your insurance company. The sooner you get the insurance company involved, the sooner you get the financials lined up for resolving your disaster.

Once you get the mitigation going you can take a breath. Getting the reconstruction part started doesn’t require an immediate decision. It requires full investigation too, so you have time to think things through.

Conclusion

Some costs can be calculated, some cannot. Nobody can calculate the loss of sentimental items destroyed by water. You also can’t calculate the loss of time and expenditure of mental and emotional energy associated with managing this recovery process. No amount of money from an insurance company can compensate for those losses

What the insurance company can do is calculate the financial impact of water damage. This is the reason you purchase insurance, to limit the financial impact. That is all that insurance can do; calculate and compensate for the financial costs. There is insurance to cover the costs of mitigation, cleanup, repairs, storing your personal belongings during the recovery, and even additional living expenses if you can’t live in your property.

Once the financial aspect has been worked out, we move on to the third party in the recovery team, the contractors hired to do the work. That will be the focus of the next post.