Water Damage Series – Part 14: Category 2 Estimate

In the previous post, talking about the category 1 loss, we introduced what the line items look like and what each column means. We talked about how each cost is included in the estimate as a line item, and why the unit prices are what they are. And we touched on a few other characteristics of the Mitigation Estimate.

In this post we’ll introduce a few more line items and unit types we didn’t see in the category 1 estimate.

Estimate Introduction Page

On the first page of the estimate, there is a section where the estimator can document things about the estimate that might not show up in the line items.

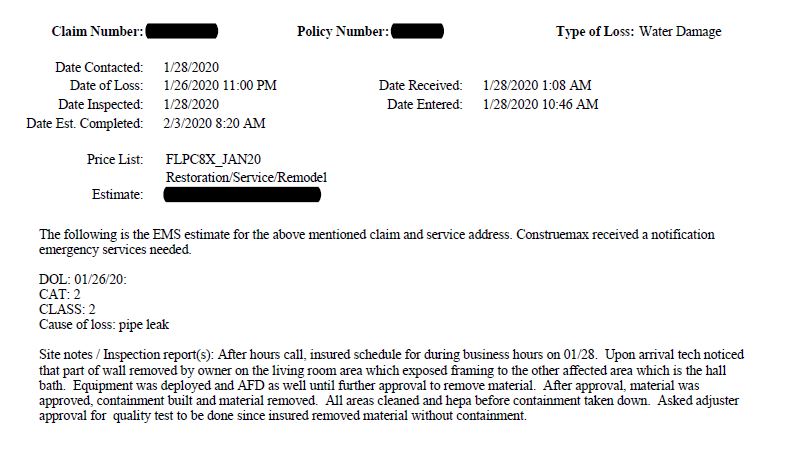

Below is an example of the bottom part of that introductory page. For purposes of privacy, names and personal information have been blacked out. The top portion of the page is nearly all private information, so it has not been included. This estimate was completed in February of 2020 as you can see in the image. The location of the loss is Panama City, Florida.

You’ll notice that there is a field labeled Price List. This changes each month. In this case, the date of loss is January 26th and the site was inspected two days later, the day our company was contacted. Therefore, the price list used was for January of 2020. The price lists are market-specific. This means that if the cost of certain materials or labor is higher in Panama City than they are in Orlando, the price list will reflect that.

The estimator can use this notes section any way they choose. It can remain blank, or it can have useful information about the loss, or even be used to include disclaimers. This particular note indicates that the loss is a category 2. It also states that it was a class 2 loss and caused by a pipe leak. This is all helpful information for setting expectations of what might be in the estimate based on how contaminated the water intrusion is and how much area is affected.

A Helpful Narrative

It isn’t necessary to document every footfall that a technician makes at a loss but helping the adjuster (in the case of an insurance claim) understand the circumstances around the loss can only aid in getting an equitable settlement from the insurance company.

In this note the estimator describes the site visit as an after-hours call. That will affect the cost of labor because employees will have to work later and when that happens, the law requires overtime rates to be paid. This increases the mitigation company’s cost.

There is a note about what the technician observed at the property. He found that the property owner had already started to remove part of the wall, exposing the home to whatever was behind that wall.

The next section indicates that equipment was deployed. That is to be expected as that is the reason for calling in the specialist. We have the commercial drying equipment needed to rapidly dry the property and protect it from additional damage.

It is not uncommon for industry jargon to be included in the estimates. We see this here with the reference to deploying AFD. What is AFD and why was it called out specifically and not just part of the equipment? AFD stands for Air Filtration Device. When the homeowner started the work themselves, they introduced the potential for contamination of the air quality in the affected area and the whole house. Without the wall being disrupted, the air filtration device might not have been added at that point, so this is called out in the introduction.

Seeking Approval

When a mitigation company comes in to clean up in a situation like this, most property owners want the insurance company to pay all the expenses. Because this is preventative measures taken to limit the extent of the loss, there is normally not any deductible for this portion of the claim. The deductible usually happens at the build-back stage.

Most homeowners will say something to the effect of “don’t do anything that the insurance company won’t pay for.” That’s understandable, but that means turning to the adjuster and asking permission to do things beyond what we were called out to do. In this case, there was a significant risk of mold infestation and the labor, equipment, and supplies needed to mitigate that risk would cost much more than just rapid drying.

Someone needs to take financial responsibility for the additional expenses, so we need someone to give us approval to move forward. The homeowner can give us permission to move forward, but who will approve the expense?

This is where the recovery team has to work together for the best outcome. Remember the recovery team? You, your insurance company, and the mitigation company.

Who Gets That Approval?

Our company will communicate our findings and recommendations directly with the adjuster. This is a service and convenience to both the homeowner and adjuster. It means that the homeowner doesn’t have to convey that information themselves. This is helpful because sometimes they don’t fully understand the findings, or are able to back them up.

It can be confusing as to why something is being requested, and because the mitigation company and insurance company deal with this sort of loss on a daily basis, we speak the same language. It is important to note that this does NOT mean that we, or any mitigation company you might hire, are representing you or acting as a Public Adjuster. We are simply communicating findings and asking if the carrier will pay additional expenses based on those findings.

The reason the approval to pay for this is so important is that the homeowner is expecting us to do nothing more than that for which the insurance company will pay. Homeowners don’t want to be stuck with a bill when they believe the insurance company is obligated to pay. Mitigation companies can’t stay in business very long if they do work where nobody is paying the costs. Lastly, the insurance company is not willing to pay for services that are not needed – what they consider ‘padding the bill’ – to get more money out of them.

So, to be fair to you, to us, and to the insurance company, we don’t move forward without approval. The approval could come from you, with you accepting financial responsibility, or it could come from the adjuster acknowledging that the additional work is necessary and covered by the insurance policy. But without approval, we stop.

New Line Items in a Category 2 Estimate

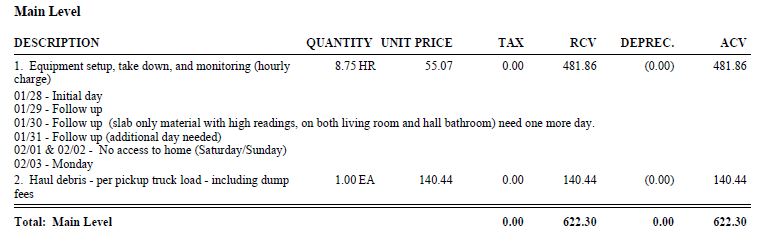

In this screen shot you can see a familiar equipment charge in line 1 with notes explaining the costs associated with the line and the days involved. But line 2 is new

Line 2 is listed to show the costs of hauling debris. Since the wall had to be removed, the debris has to go somewhere. As the homeowner, you’re expecting the mitigation company to haul it away, and so we do.

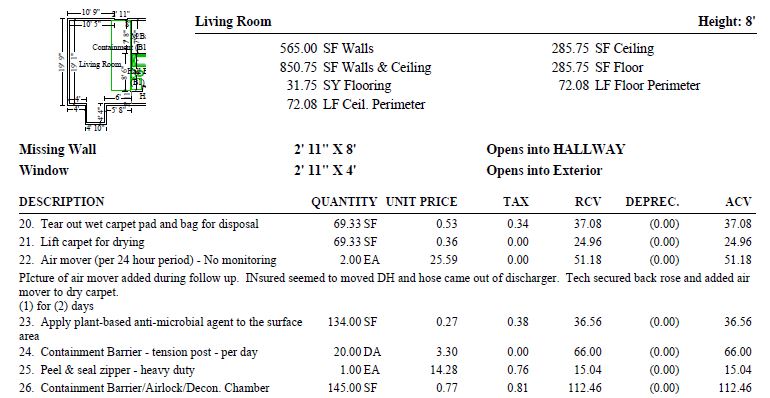

Good Estimates List Each Room Separately

To simplify the estimate, it is broken down by each room, or in the case of a hallway, the area that is affected.

The numbering of the estimate continues where the previous affected area left off so it can make it much easier when discussing the estimate with your technician or adjuster by just referencing the line number.

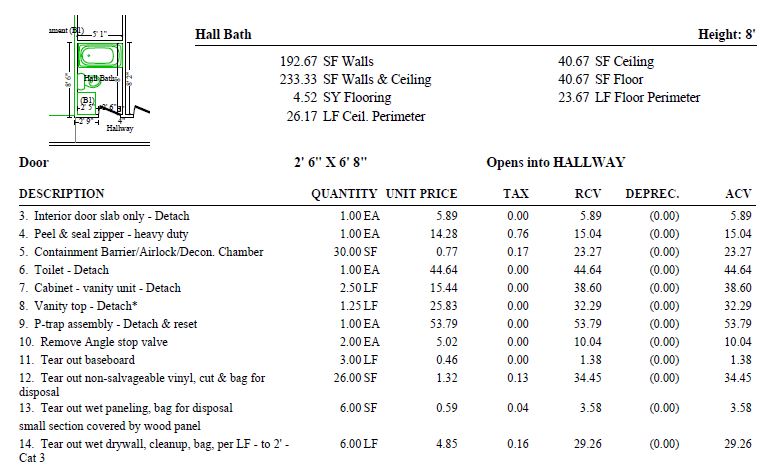

In addition to the line numbers and the descriptions and prices of those line numbers, you will usually also see a sketch and the dimensions of that room. In the following image you see the room labeled at the top and the height of the ceiling listed. Below that, the surface area is shown in square feet (SF) or square yards (SY).

There are also linear feet (LF) shown for things that are more appropriately measured that way, such as the perimeter of a room or lengths of baseboard and trim.

Detach & Reset

Looking at these lines, one by one, you’ll notice that some lines reference materials such as line 4 with the Peel & seal zipper and line 5 with the containment barrier. But you’ll also see lines like 3, 6, 7, 8, and 9 referencing Detach; line 9 says Detach & reset.

To detach means to remove the item or detach it from its original installed location. In these lines, the items need to be moved so the restorative drying process can happen at a rapid rate. If water is trapped behind cabinets, under a vanity top, or behind baseboards, they might dry without removing them, but they are much more likely to cause damage or grow mold because they stay wet too long.

Line 11 says Tear out baseboard and doesn’t use the term detach. The reason is, if it is unsalvageable, it will just need to be torn out and discarded. If the item is salvageable, then it will need to be detached and not discarded. At some point, it will need to be reset or reinstalled again.

Line 9 references the reset: 9. P-trap assembly – Detach & reset. Before completing the mitigation and dry out, the P-trap will be reset. In the case of the other items, they will need to be reset by someone during the restoration phase. This is just the dry-out and cleanup phase. It means that the room will be unusable until the restoration is complete, but mitigation is all about arresting further damage and removing contaminants and damaged materials that are unsalvageable. The build back is a separate phase and therefore a separate estimate.

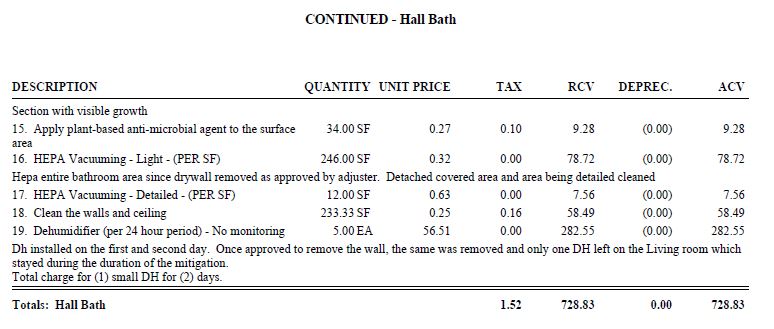

A Single Line With Category 3 Contaminants in a Category 2 Estimate

This section of the estimate on the Hall Bath has enough lines to overflow onto the next page. It just happens to be the one line with Category 3 contaminants.

Line 14 is continued from the previous page. The line in total says:

14. Tear out wet drywall, cleanup, bag, per LF - to 2' -

Cat 3

Section with visible growth

This estimate is for a category 2 loss. This line references a Cat 3 section. This would stand to reason if you’re dealing with damaged drywall behind the toilet. But with a 6 foot x 2 foot section of drywall, that isn’t enough to change the overall category of the loss, so it is referenced this way.

Did I Mention Cleaning?

I just mentioned that during this water damage mitigation job we are drying out the property, removing unsalvageable materials, and cleaning. We see the first references to this here in the Hall Bath.

Lines 16, 17, and 18 reference cleaning. The walls needed to be cleaned with a HEPA vacuum. The ceiling too required cleaning. Because there is contamination from the water loss, it needs to be cleaned.

Part of that cleaning process includes applying a plant-based anti-microbial agent. That is listed in line 15.

Don’t Try This at Home

The reason to hire a professional mitigation company is to ensure that the job is done right. In line 22 below we see that somebody did try it at home, and it didn’t go well.

This line documents that the homeowner moved the dehumidifier in the living room causing the hose to become disconnected. The consequence of that is that the drying process was extended. To make up for that there was a new piece of equipment needed.

That line alone added $51.18. With additional days of drying, other lines will be affected as well. Lines 24 and 31, a tension post and an air scrubber, are pieces of equipment charged by the day.

Containment Is Key to Preventing Additional Damage

In these lines above we see the references to containment. This containment is made with plastic wall barriers like the one in this image. It is held in place with tension rods and tape.

The purpose of the containment is to prevent any debris that is being removed from spreading dust throughout the property. But it’s not just dust, but mold spores as well. Wherever you have water damage you run the risk of mold beginning to grow and that must be contained.

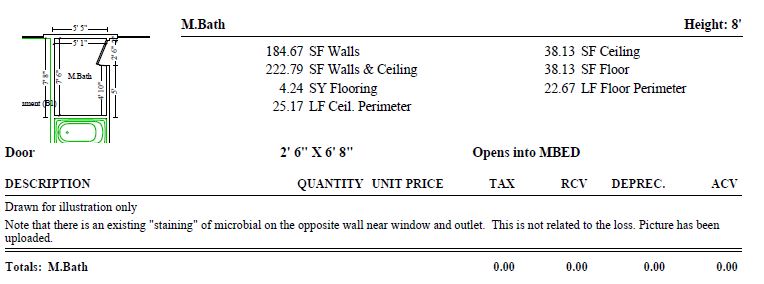

Sometimes Just For the Record

There are times when there are rooms that are not affected, but very easily could be. If one room is affected, it is important to look at the room on the other side of the wall. Of course, if that other room is affected too than it needs to be mitigated as well. But what if it’s not? Just move on and forget about it right? Not necessarily.

Including the sketch in the estimate and noting that there is no damage in the room on the other side of the wall gives completion to the question of how widespread the damage is. Without this, there might be lingering questions about whether or not there was any additional damage.

Coming Next…

Every estimate is unique. It has different needs in terms of what line items will be required, how long the dry out will take to complete, how many rooms are affected, and on and on. In the next post, we will look at an estimate for a category 3 loss.