Water Damage Series – Part 13: Category 1 Estimate

Understanding the processes of dealing with water damage is a good thing and should help you get sleep at night. We hope that the previous posts in this series have been helpful in gaining or solidifying that understanding.

Understanding the written estimates of the costs incurred is a different matter altogether. This post is intended to introduce you to what an estimate might look like and what some of the line items would mean.

What Is on an Estimate

Construemax writes its estimates in a program called Xactimate. Most insurance companies require estimates written using it, or a program very similar. The software is very powerful. It creates an estimate with a clean and consistent format. But it also has a built-in price list for all the different services needed for both the water mitigation phase and the reconstruction phase of the property restoration.

The estimate will typically include sketches, measurements, line items, and prices of each line item. Some estimates may include all of these things, and some may be printed with only some of them, a scope of work.

How Is an Estimate for Mitigation Different?

What makes an estimate for water or mold mitigation different from most estimates is that it is more like an itemized bill after the fact than an estimate of what it will cost to do the job before they start.

When the mitigation is complete the technician may have removed drywall, carpet, and insulation. The job of putting that all back together again is straight forward. The reconstruction team will install insulation, drywall, and carpet. Then to do the finishing work they will need to mud the seams of the drywall, apply texture, and paint.

The costs of each of these tasks can be estimated by measuring how much of each material type is needed and through experience, the amount of time needed to complete the work. It’s not as straight forward with the mitigation part of the water loss.

Restorative Drying Has Too Many Unknowns

The Principles of Drying Your Home or Business uses equipment to manipulate the atmosphere of the room. We do this to accelerate evaporation. While technology is very helpful, both the existing conditions inside and the weather outside the property, including humidity and temperature, will impact how efficient the equipment is.

Where the drying process might be quick during one time of the year, it could be much longer during another. Additionally, how much water was absorbed by the building materials is unknown at the start. Some of the water will have been removed when you remove carpet or damaged drywall, but wood floors and studs, and concrete floors might have absorbed quite a bit of water which will take longer to dry.

This means that a technician can’t say how long it will take, or how much equipment might be needed. The variance between what one might estimate in advance of doing the job, and what the actual requirements are is large enough that in the end, the most effective estimation approach is to do the itemization after the fact. We still call it an estimate since it uses the same software and format as every other estimate.

Simple Category 1 Estimate

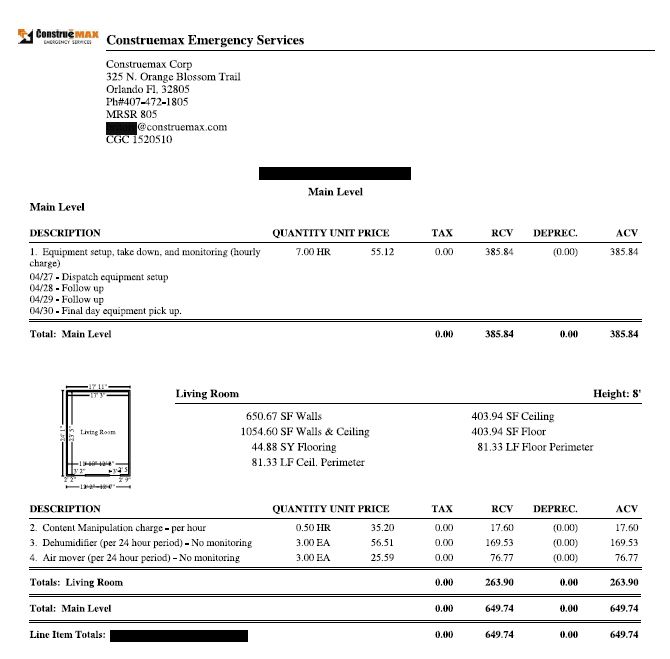

Below is a page from a simple category 1 water loss. The whole estimate is a nine-page document, and this is the third page. The other pages include information about the property, the circumstances around what caused the loss, measurements, summaries and so forth. This page is the core of what you’re interested in in an estimate.

The black bars on the page block out personal information and are not relevant to the loss.

What Things Mean on the Estimate

This estimate is about as simple as you can get. The cause of the water damage was a broken window that allowed rain to come in and get the floor and walls wet. Because it was a very isolated area, as seen in the sketch, there is only one level and one room identified.

Each line item has:

- Description – Of course, this describes what the line item is, and sometimes what it is not. In the case of this example, you can see that lines 3 and 4 state “No monitoring”, i.e. what it is not.

- Quantity – Different line items require different units of measurement. This will include not only the number but identify the unit used.

- Unit price – Once it is clear what the unit is from the quantity column, the unit price is self-explanatory.

- Tax – Some things have sales tax, some do not. This will vary from one state to another. In Florida, most services are not charged with sales tax, but materials are.

- RCV – This is Replacement Cost Value. It is an insurance term referring to the actual cost of replacing something that is lost, stolen, or damaged.

- Depreciation – This is a loss in value of something because of time, wear and tear, or obsolescence.

- ACV – This means Actual Cost Value. Again, an insurance term, and it means the value of the item with depreciation taken into consideration.

Understanding This Estimate

Again, this estimate is for a category 1 loss. Since the water is from rain and came into the property directly through the broken window, there are no building materials or ground for it to come into contact with before finding its final location on the floor and walls of the living room. That makes the water source clean.

Because the property owner acted quickly, the amount of time the area was affected was not long enough for it to become a category 2 loss.

In this estimate, because it is just including the cost of services, the RCV and ACV are exactly the same. They reflect the cost of the service. The DEPREC. section doesn’t apply because depreciation will only apply to physical things that are being replaced. In a different estimate, where materials are actually removed, the depreciation section will apply in the restoration estimate for the build back. You wouldn’t expect to see it used in the mitigation estimate.

A Word About Costs

The mitigation technician is at your property to do a job. They get paid to do that job because, like everyone, they have bills to pay. If you’re an employee or own a business, you expect to be paid for your labor or your products. In business, you will price your products and services so that your costs are covered, and you have something left over for you. Of course, there is no revelation here, it’s just a reminder.

The point is that any costs associated with doing the work will be accounted for in the numbered lines of the estimate. It may seem insignificant for the estimate to include a $1.38 line item and may seem like nickel-and-diming, but the costs add up and they need to be paid.

Some of those costs are absorbed into the price of the product like marketing, accounting, and uniforms. But some costs are only incurred by virtue of doing a specific job. For example, the Personal Protective Equipment (PPE) needed for a category 1 loss may be very minimal, but the PPE needed to clean up a category 3 loss is substantial. Therefore, that substantial cost, that would not otherwise be incurred, except for working on your job, is included in the itemization of costs, or this estimate.

Keep this in mind as we review each of the lines of this estimate.

Line 1

Details for this line are listed. In this case, the details identify the days where the charge applies. It first lists the date of when the equipment was setup is shown and the task identified.

Next, It lists two days of ‘Follow up’. It is a normal practice for the water mitigation technician to visit the site each day, measure progress, make adjustments, and record the day’s activities.

The job of the technician is to determine what equipment is needed to dry out the property, and then remove the equipment when it is dry. Since every situation is different, the only way this can be done effectively is to monitor daily.

As you can see, by the third day of monitoring the water technician found that the moisture levels were normal again and that means drying is complete. The equipment was then removed and the job was ready to be estimated.

Line 2

Unless the property is vacant, there is usually something in the room that is wet that needs to be moved. In a living room, there could be furniture like couches, recliners, coffee tables, bookshelves, and so many other things. Look around your own living room and see what would need to be moved if your walls and floor got wet from rain.

All these things need to be moved. In the case of this loss, there was only a ½ hour charged. That means there wasn’t very much. But on bigger losses, it can be a lot of things that need to be moved. In the industry, those items are referred to as ‘Contents’. They are the contents of the house.

Very often the contents of the house are also damaged and there is insurance coverage to compensate you for that. That compensation is not going to be found in this estimate. But if those personal belongings need to be moved for the drying process to be performed, or carpet to be removed, then the estimate will show that charge.

Lines 3 and 4

These two items are the equipment used for the dry out. When you look at the quantity is shows 3.00 EA (or 3 each). This is because the equipment was at the property for three days. Rather than list each of them three times, the quantity is used to reflect three 24 hour periods as identified in the description section. If there were two air movers used for all three days you should expect it to reflect 6.00 EA, and then in notes immediately below the line, it would explain that there were 2 air movers for 3 days.

The description section also states No monitoring. This is because this charge is only for the usage of the equipment. The cost of monitoring the equipment uses a different unit, it uses an hourly rate vs a 24 hour period. The cost of monitoring is included in line 1 along with the setup and takedown.

A Word About Unit Prices

If you are a business owner, especially with employees, you understand that there are many costs above a simple hourly rate or cost of goods. You deal with this every month. Most non-business owners understand this too, but I want to take a few lines to address this.

A unit price of $55.12 might seem like a high rate for a technician. You might say, “wow, I don’t make anywhere near that much an hour!” But this hourly rate is not the tech’s salary. That rate has to cover the cost of not only the take-home pay for the hours at your property, but also the travel time, as well as employee expenses such as taxes, workers compensation, and benefits. There is also the cost of the vehicle that is used to transport the technician, equipment, and supplies. Those costs include gasoline, insurance, loan payment, maintenance, and on and on.

The rates used for equipment will include the costs of cleaning them each time they are returned to the warehouse after a job. Filters have to be replaced, and the equipment needs to be fully inspected to ensure safe usage at future jobs. If the equipment isn’t functioning properly it will need to be repaired. Of course, the cost of replacing the equipment when its useful life is over also has to be considered.

The point here is that even with breaking out each cost by line item, each item itself has many hidden costs, that cannot be itemized.

Getting Estimates From Different Companies

Regardless of what company writes up the estimate, if they are using the Xactimate or other software as required by insurance companies, the estimates will be the same for each line item. The differences between the final estimate numbers between two companies would come from one company using more equipment than another, taking a different amount of time to setup, take down, and monitor the equipment, or one company might forget to include expenses whereas the other is thorough.

This estimate is very simple. Almost as simple as it can get with only four lines. But looking at another estimate, I see a category 2 loss, one that has 33 lines and 4 times the cost. With that many lines it is easy to miss an expense and fail to bill for it.

Conclusion

Estimates for water damage mitigation can have a lot of information on them. Once you are familiar with them, understanding them isn’t too bad. If you ever have a question about what you see on your estimate, you can ask the person who gave it to you. Whether it is the person who gave it to you or your insurance adjuster, there will be an explanation for each line.

In the next post we’ll use an estimate from a category 2 loss which will introduce line items you might not have thought of to itemize in an estimate.